The function of economic forecasting is to make astrology look respectable.

John Kenneth Galbraith

Canadian-American economist, 1908-2006

03 February 2023, Graham Harrison

John Kenneth Galbraith

Canadian-American economist, 1908-2006

As Harold MacMillan is reputed to have said, the greatest difficulty comes from “Events, dear boy, events”.

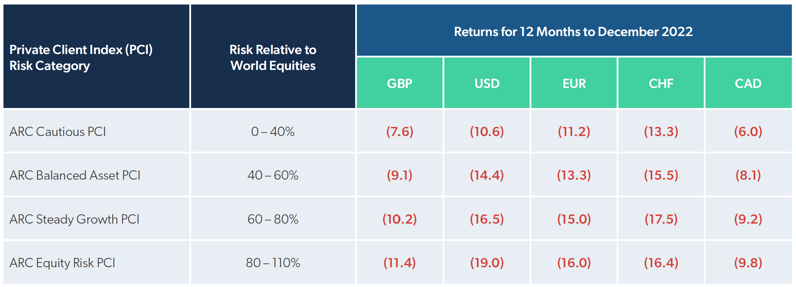

2022 was a year when events made the art of investment even more difficult than usual. A combination of factors including the war in Ukraine, inflation and slowing global growth triggered falls in the value of most asset classes over 2022. Thus, multi-asset class portfolios delivered negative returns for the vast majority of private client investors as the table below illustrates.

With falls in almost all asset classes, the notable exceptions being energy and commodities, there were very few opportunities for investors to avoid losses. Indeed, sharp rises in government bond yields meant that traditional safe haven assets failed to provide capital protection.

Looking across the five PCI currencies, in local currency terms losses were highest for USD investors. However, that masks significant currency moves during 2022. For example, the US Dollar appreciated against most other currencies; versus Sterling it ended the year up 12% and at one stage was up 20%.

The Real Picture

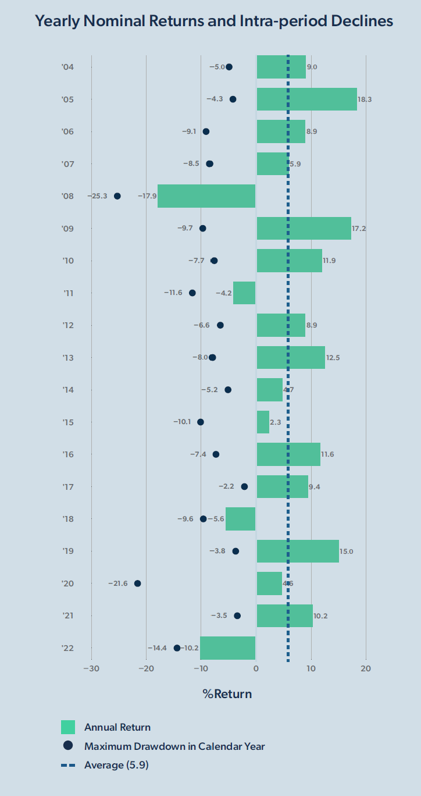

So, how has the performance of a typical private client portfolio in 2022 compared to that experienced in previous years?

By way of illustration the chart below plots calendar year returns and maximum drawdown in each calendar year since 2004 using the daily estimated series for the ARC Sterling Steady Growth Private Client Index, the PCI series with the greatest number of constituents.

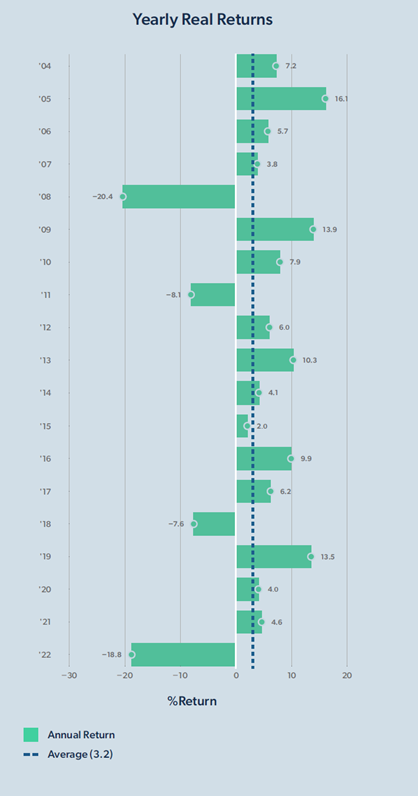

However, the raw data set out in the previous chart does not tell the full story. Inflation has dominated the headlines in 2022 as, across the world, it reached double digit levels and proved surprisingly resistant to the monetary policy actions of central banks. For investors accustomed to low and stable inflation, its impact on the real value of their wealth may not have been immediately apparent.

The chart below plots the same calendar year returns adjusted for inflation.

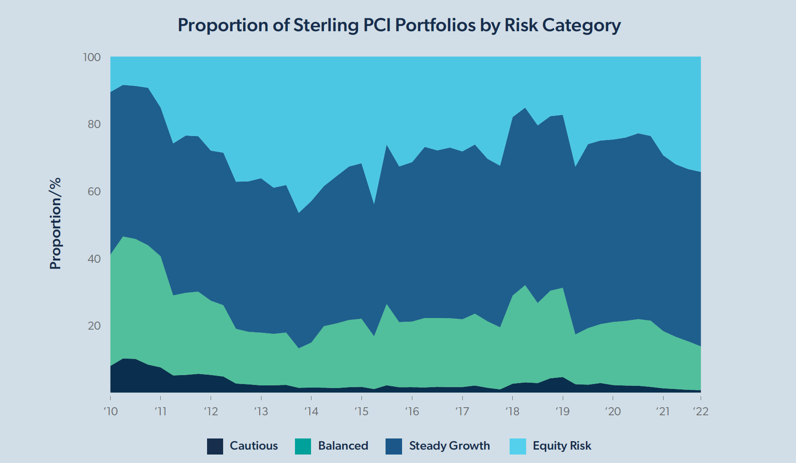

The ARC PCI series are divided into four risk categories, with the two lowest risk categories, Cautious and Balanced Asset typically having less than 55% in equity markets and a sizeable allocation to bonds and other assets.

Over the last decade or more, during the financial repression that followed on from the Global Financial Crisis, bonds changed from offering investors a risk-free return to promising them return-free risk. Delivering not just negative real returns but also negative nominal returns, private client discretionary managers sought to minimise exposure to fixed income amidst chatter that a conventional multi-asset class portfolio was no longer relevant or indeed suitable.

The ARC PCI universe reflected that shift in portfolio construction with the percentage of private client portfolios falling into Cautious and Balanced Asset categories declining. This trend may well have reached its apotheosis in 2022, with the proportion of portfolios falling into the Cautious category falling from around 10% at the end of 2010 to below 1% at the end of 2022. Taking the two lowest risk categories together, the percentage has similarly fallen from around 40% of portfolios to around 15%.

2022 proved to be the year when fears that a perfect storm of rising inflation and the normalisation of bond yields blew away the value of bonds.

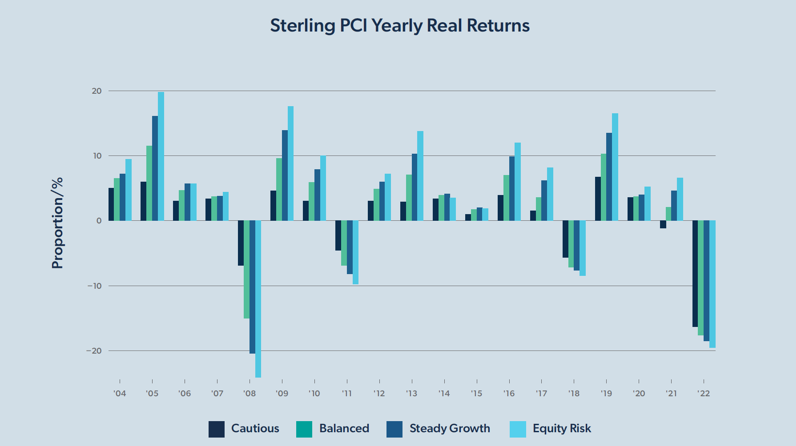

It was a year when caution was not rewarded. The chart below plots the annual performance of all four Sterling PCI risk categories over the last 19 years in real terms. What is clear is that 2022 was the worst year for Cautious portfolios by a considerable margin and Balanced Asset portfolios also experienced their worst year. The average Cautious portfolio fell by 16.4% in real terms; that is nearly three times the magnitude of real losses in 2008, 2011 and 2018, while Balanced Asset portfolios fell in real terms by nearly 18%, more than the loss experienced in 2008 of 15%.

The same pattern is evident in the other PCI currencies, albeit that the worst destruction of real capital for Cautious investors was experienced by Sterling denominated portfolios.

Looking to 2023 and beyond, it seems likely that investors will face ongoing uncertainty: a resolution to the conflict in Ukraine appears to be remote; geo-political tensions remain significant; slowing global economic growth may well turn into localized recessions; inflation may well prove stubborn as supply chain disruptions continue and labour shortages remain; and corporate earnings will surely come under significant pressure.

However, uncertainty also creates opportunities for discretionary managers and, with equity valuations becoming more attractive and real bond yields improving, there is hope that 2023 will be a better year for investors.

It also seems likely that portfolios exhibiting a risk profile of the Cautious or Balanced Asset categories will see something of a renaissance as bonds begin to offer the prospect of positive real returns. For a decade or more it has made sense for investors to throw caution to the winds with only equities appearing to offer a positive real return. That has changed and once again it has begun to make sense to consider bonds as a viable investment class.

A full list of Data Contributors to ARC PCI is available at www.suggestus.com

For those private client investors who wish to place their 2022 performance into peer group context, or indeed examine a longer period, the ARC Performance QuickCheck tool is a free, simple, independent analytical tool designed to perform a ‘health check’ on the performance of a discretionary portfolio.

Visit www.suggestus.com or search in your phone’s app store for Suggestus to get started.