The anything supper

Dr James Cooke, CFA

Director of Research

Everything in moderation, including moderation.

Oscar Wilde

Anything, with chips

In Scotland, an anything supper means exactly what it says. You can have almost anything, as long as it comes with chips. The chips are comforting, familiar and filling. They are also non‑negotiable.

There is generosity in the tradition. It is food rooted in community rather than optimisation. But eaten too often, chips crowd out balance. Over‑reliance, not the ingredient itself, is what causes harm.

That distinction maps neatly onto markets.

Global equity markets appear varied. Thousands of securities, sectors and strategies. Under the surface, ownership and returns are increasingly concentrated around a narrow set of companies, technologies and capital providers. Different labels. The same base.

Fries with everything

The numbers are instructive.

The US now accounts for close to half of global listed equity value, up from roughly 30% 15 years ago. Within that, a small group of mega‑cap technology firms dominates index returns. Passive ownership has reinforced the pattern. Large asset managers hold meaningful stakes across hundreds of companies, often simultaneously across competitors.

By 2022, fewer than a quarter of MSCI All Country World Index constituents were widely held. A growing share of market capitalisation sat in controlled or tightly owned companies. In practice, many portfolios rely on the same growth drivers, the same profits and increasingly the same technologies.

For years, this paid off. Concentration reduced career risk, amplified returns and rode genuine technological progress. The mistake is not believing in the technology. It is assuming that belief alone guarantees investment returns.

When growth burns calories

Sandy Nairn’s old insight still applies. Transformational technologies change the world. Early investors rarely capture the long‑term rewards. The pattern repeats. Breakthrough. Capital rush. Overinvestment. Disappointment.

When growth is explosive and uncertainty high, concentration can make sense. Like a young body burning calories fast, the system can absorb heavy intake. Early‑stage AI looked like that. Winners were separating. Optionality was high.

As technologies mature, metabolism slows. Growth persists but becomes less uniform. Capital intensity rises. Competition tightens. Regulation appears. The same exposure that once fuelled returns starts to create drag.

AI is moving into infrastructure. That does not diminish its importance. It raises the bar for valuation discipline and diversification. Structural growth rewards selectivity, not blanket exposure.

Extra chips in the system

Semiconductors sit at the centre of this shift. Industry value could double this decade, driven by AI, data centres and advanced computing. Growth alone is not the risk.

Production is highly concentrated. Taiwan produces more than 60% of global semiconductors and over 90% of the most advanced chips 2. One firm dominates advanced manufacturing capacity.

If chips are the engine of the digital economy, the global economy is relying on a single, vulnerable workshop.

This is not abstract risk. Any disruption would ripple through technology, autos, defence and energy systems. The effects would be immediate and global. Governments know this. Industrial policy and reshoring efforts are accelerating. But advanced fabrication takes years and tens of billions in capital. Capacity cannot be conjured on demand.

When the chips are down

This is where the metaphor stops being playful.

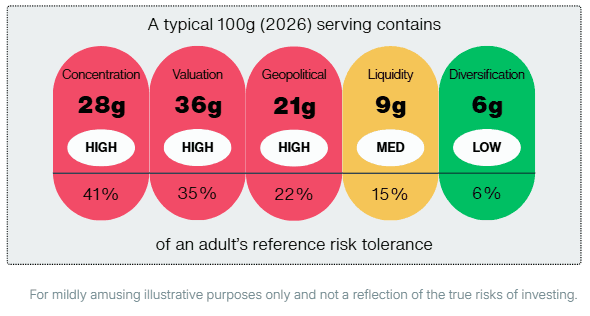

Concentration today is not just a portfolio construction issue. It is systemic. A narrow set of companies, technologies and geographies now explains a large share of global equity returns and future expectations.

That configuration feels efficient until it is not.

If this were a food label, the warnings would be clear. Heavy reliance on a single ingredient. High sensitivity to supply disruption. Limited resilience if conditions change.

So what?

This is not an argument against chips. Either kind.

Semiconductors are indispensable. US technology firms are exceptional businesses. Passive investing has lowered costs and broadened access. None of that is in dispute.

The risk lies in building portfolios that cannot cope when the shared assumption breaks.

Diversification is not about owning more holdings. It is about owning genuinely different outcomes. Just as good nutrition is about balance rather than abstinence, good portfolio design recognises when a convenient staple has crowded out too much variety.

An anything supper still has its place. Best enjoyed occasionally, knowingly and without pretending it is a balanced diet. Modern portfolios would benefit from the same restraint.

This article is provided for information purposes only and does not constitute investment advice or a personal recommendation. ARC accepts no liability for any action taken or not taken in reliance on this content. Click here for regulatory information, third-party data terms and full disclosures.