Mega IPOs, familiar behaviour

Dr James Cooke, CFA

Director of Research

They say the next big thing is here, that the revolution's near

From “History Repeating” by Propellerheads featuring Shirley Bassey (1997)

Markets do not move in neat cycles, but behaviour often repeats. When confidence is high, capital is easy and stories are compelling, investors tend to pay up. That works, until it does not.

We have a genuine technology shift. Markets are trying to price that shift while much of the commercial upside still sits in the future. AI usage is widespread and increasing, spending is real, infrastructure is being built and revenues are visible.

Transformative technologies have come before, from canals and railways to electricity and the internet. Each delivered lasting economic benefits. Each also attracted large amounts of capital when confidence was strong and the investment story felt hard to resist.

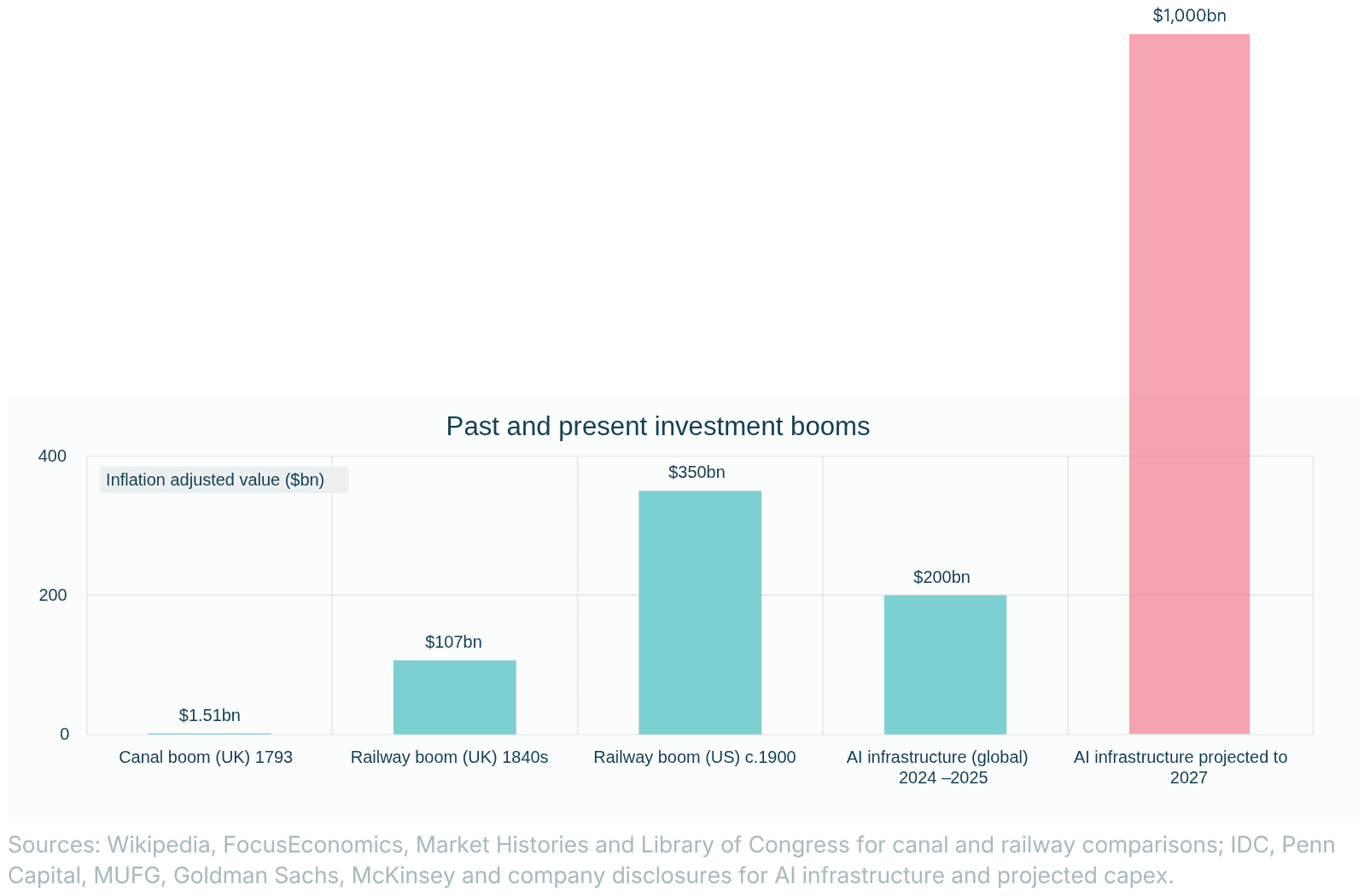

Past and present investment booms

The chart below puts current AI infrastructure spending in context. The scale is already significant and projected to rise sharply by 2027.

Heavy investment can accompany real economic change. It can also coincide with periods when expectations run ahead of what later proves achievable.

Much capital has already been committed in private markets to businesses operating in and around AI. That changes the role of the initial public offering (IPO). Earlier valuations meet a broader public market test at that point, often after years of private funding and rising optimism.

Companies tend to list when conditions favour sellers. Valuations are usually high, liquidity is abundant and demand is broad and confident. Historically, high issuance by operating companies clustered around the dot com period into 2000, while financial issuance peaked into 2007.

A few businesses thrive. Most do not. Many of the weaker businesses in this cycle may still be in private hands, without any public test of their market values. The echoes of history are familiar: a dominant narrative, strong market performance and a backlog of companies ready to list. The differences matter too. The companies now expected to come through are larger, more mature and potentially more important to the wider market. Demand is also more institutional than retail.

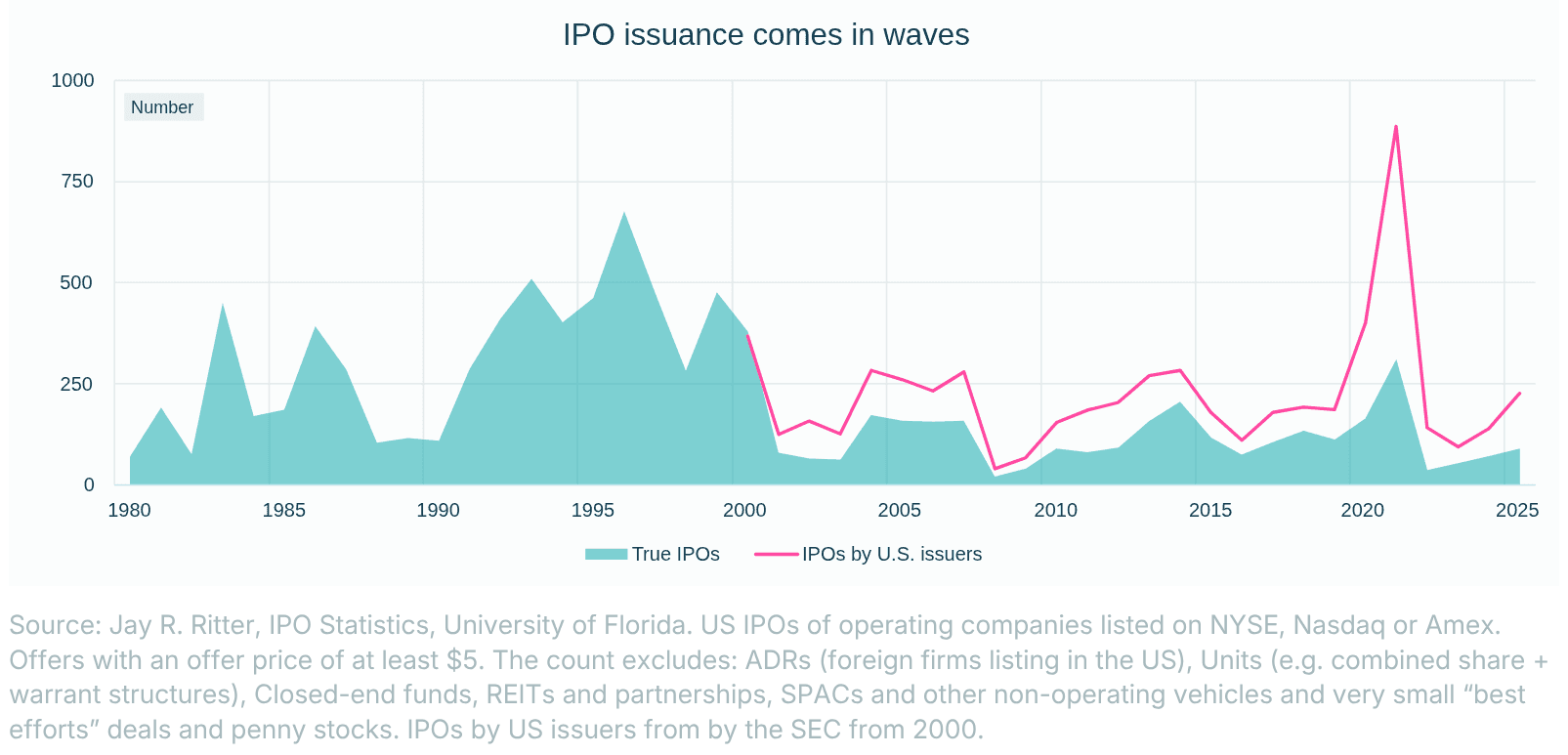

IPO issuance and what it shows

At the peak of the dot com boom, issuance was broad. Hundreds of companies came to market, raising tens of billions. The next cycle may be narrower and far larger in value. SpaceX alone could raise between $40bn and $80bn at a valuation approaching $2tn. OpenAI is targeting a valuation above $1tn, with proceeds around $60bn. Anthropic may follow at similar scale.

That difference is important. A small number of businesses may account for a very large share of the value, even if only a modest portion of their equity is floated. Public listing becomes the point where private market enthusiasm meets public market price discipline.

What matters for investors

It can be tempting to treat the noise around IPOs as a call to action. In practice, that is rarely the most useful response. IPOs are designed to be oversubscribed. Greenshoe options, allocation dynamics and early trading help create a newsworthy debut. None of that guarantees an attractive long-term entry point.

A few guiding principles are more useful. Stay exposed to the trend, but reduce concentration risk. Some of the strongest returns in recent years have come from AI-linked companies. Broad market exposure captures that naturally, while rules-based dynamic approaches can adjust exposures over time.

Let processes do the work

Late-cycle environments tend to expose inertia. Positions drift, asset allocations drift with them and concentrations build unintentionally. Decisions get postponed. A simple structure helps: disciplined rebalancing, rules-based approaches and dynamic passive strategies. None requires perfect timing. They help portfolios adjust as markets move.

The practical point is straightforward. Investors do not need a precise call on when enthusiasm peaks. They do need to make sure portfolios are not being pulled into unintended concentration by strong recent performance and a compelling narrative.

Avoid dependence on one part of the market

The broader point is to avoid becoming too dependent on one theme, one style or one narrow part of the market. That risk tends to build gradually in periods of strong performance, especially when one story dominates attention.

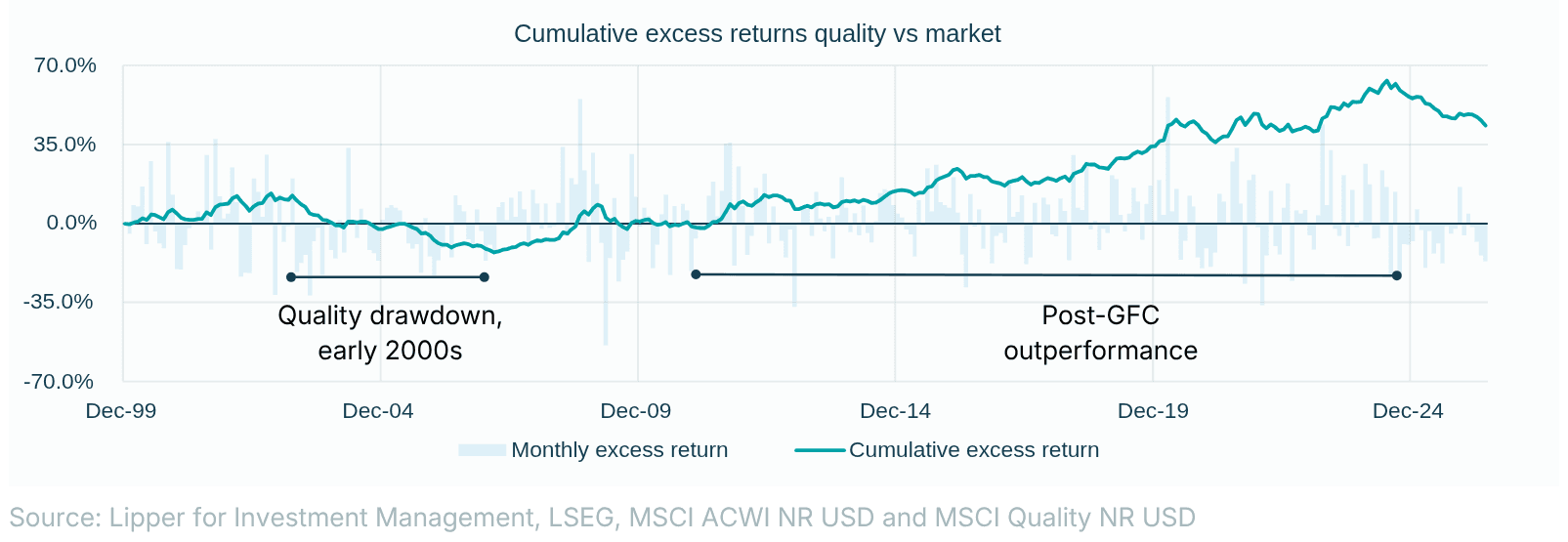

Before the dot com unwind, value had been left behind. When leadership turned, it moved quickly. The chart below makes a similar point in a different way. Quality can lag for extended periods when markets favour excitement, momentum and long-duration growth. It can also recover strongly when conditions become less forgiving.

Quality lagged during speculative leadership, then recovered when conditions changed. A diversified portfolio does not need to predict the exact turning point. It does need enough breadth to cope if leadership changes.

Final thought

There is a familiar instinct at moments like this. Nothing looks obviously wrong. The buildout is real. The opportunity is clear. That is what gives the story its force. Expectations stretch in that environment, often through confidence rather than panic. Then, reality starts to matter again.

Stepping off the floor entirely can be costly. Staying on without noticing the exits can be worse. This time is not exactly the same, but it is close enough to justify caution. Investors do not need to call the turning point perfectly. The discipline is to stay invested, stay diversified and make sure that, if expectations do begin to reset, the portfolio is still where it was meant to be.

The most practical step is also the simplest: revisit your asset allocation.

does it still reflect your risk tolerance?

are you comfortable with current concentrations?

has your time horizon shifted? Markets change quickly. Objectives usually do not.

This article is provided for information purposes only and does not constitute investment advice or a personal recommendation. ARC accepts no liability for any action taken or not taken in reliance on this content. Click here for regulatory information, third-party data terms and full disclosures.