A world in motion

Dr James Cooke, CFA

Director of Research

The decade, the year and the road ahead

A year is just the time the Earth takes to circle the sun. But the decade has been far less orderly than that annual orbit.

War returned to Europe and unsettled energy and security. Famines resurfaced in fragile regions. A plague by any other name tested health systems and policy everywhere. Shipping routes were disrupted. Technology leapt forward while climate records fell. The sense that shocks can arrive from any direction became part of daily life.

Investors still hope for no surprises; the decade kept delivering the opposite.

2025 in brief

Trade policy and sea lanes dominated.

The United States introduced broad tariff measures. While well telegraphed, the game‑show style announcement with questionable arithmetic delivered a negative shock.

Effective rates shifted through the year as deals and delays took effect, and uncertainty remained high, even as the IMF nudged its growth path slightly higher while warning that tariffs could still cloud inflation and activity. Firms adjusted prices and procurement to cope and investors watched margins and pass‑through.

Attacks on commercial shipping kept the Red Sea and Suez risky. Major lines detoured around the Cape of Good Hope. Asia to Europe transits lengthened by roughly one to two weeks. Insurance premia rose and lead times stretched. Adaptation at the quay became adaptation at scale across supply chains. The year left markets with a few bruises that won’t quite heal.

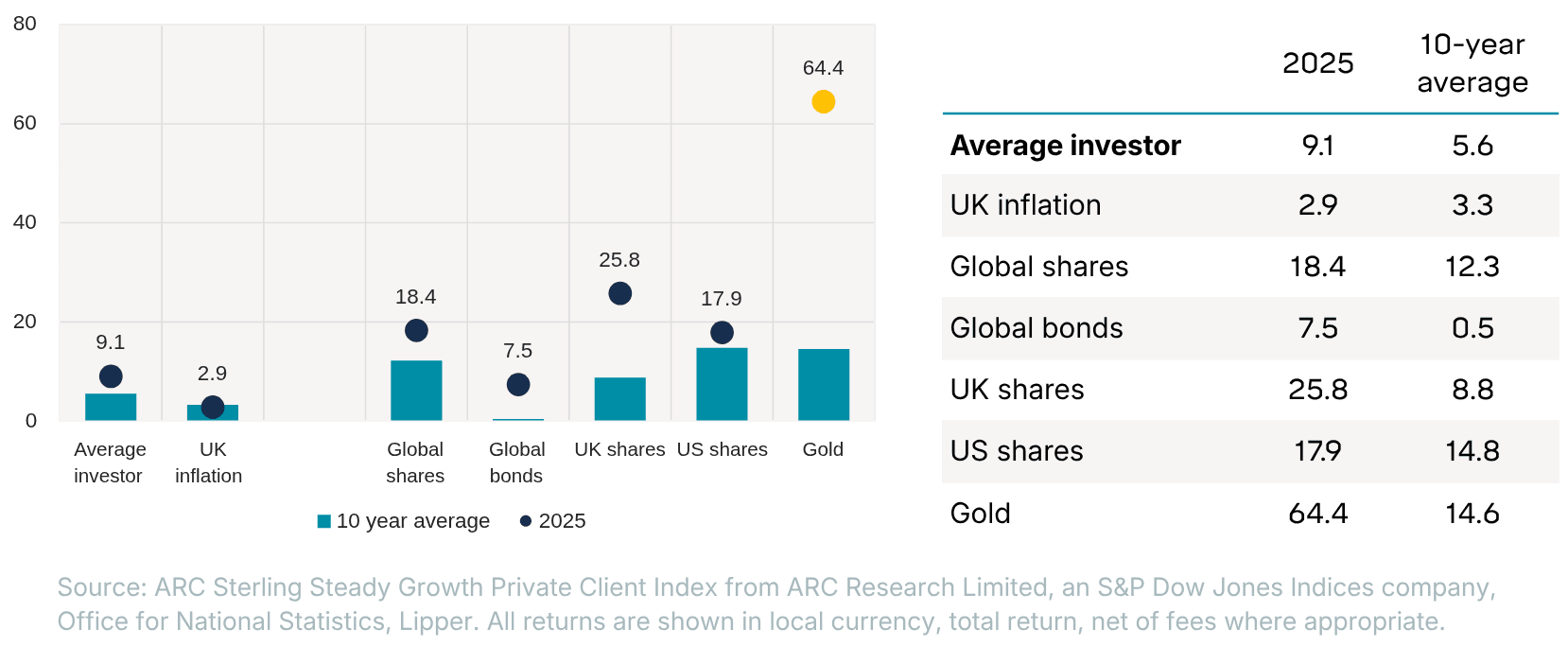

Despite all this, returns overall were well above average levels with global equities delivering 18.4%, global bonds 7.5% and the average investor (ARC Sterling Steady Growth Private Client Index) seeing a return of 9.1%. Real values of assets are now around those seen pre-covid.

Investors

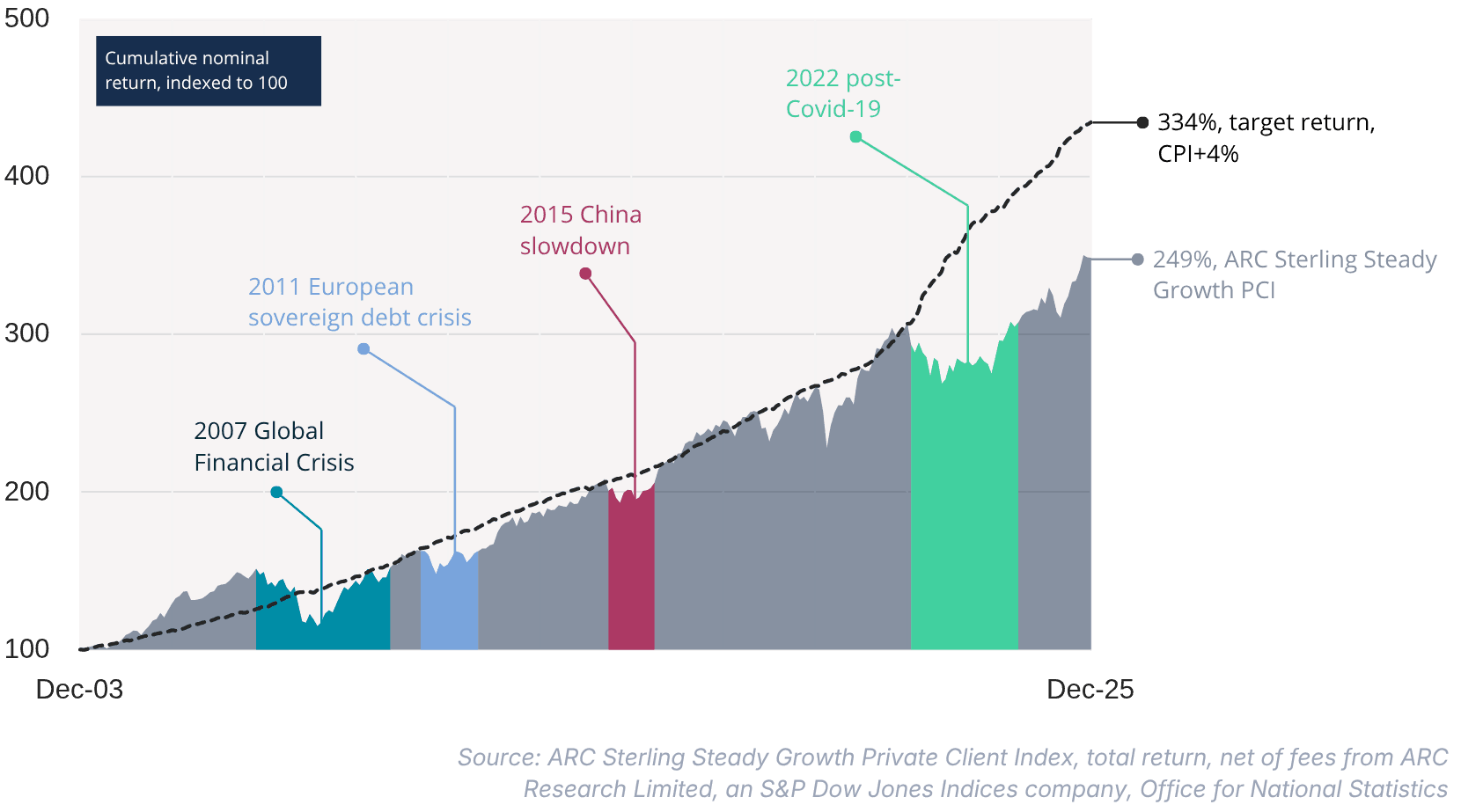

Despite economic challenges and geopolitical events, returns in 2025 were much better than anticipated. The graph below shows average ARC Sterling Steady Growth Private Client Index returns since 2003. The ARC Wealth Indices are constructed from over 350,000 portfolios from 139 investment management firms.

Regimes with losses greater than 10% that took more than twelve months to recover are highlighted. These include the 2007 Global Financial Crisis, the 2011 European sovereign debt crisis, the 2015 China slowdown and 2022 post-Covid-19.

Lasting only 10 months in our terms, the 2020 Covid-19 pandemic does not show up as a major negative event for investors.

This was because, in response to the pandemic, global central banks collectively created more than five times the amount of new money issued during the financial crisis.

There was however a hangover effect.

The 2022 post-Covid-19 period was characterised by monetary conditions reversing, that is central banks raising interest rates and moving from quantitative easing to tightening, as well as an increase in inflation. Some of this was due to Russia’s invasion of Ukraine and an increase in energy costs.

In nominal terms, many portfolios are now at all time highs.

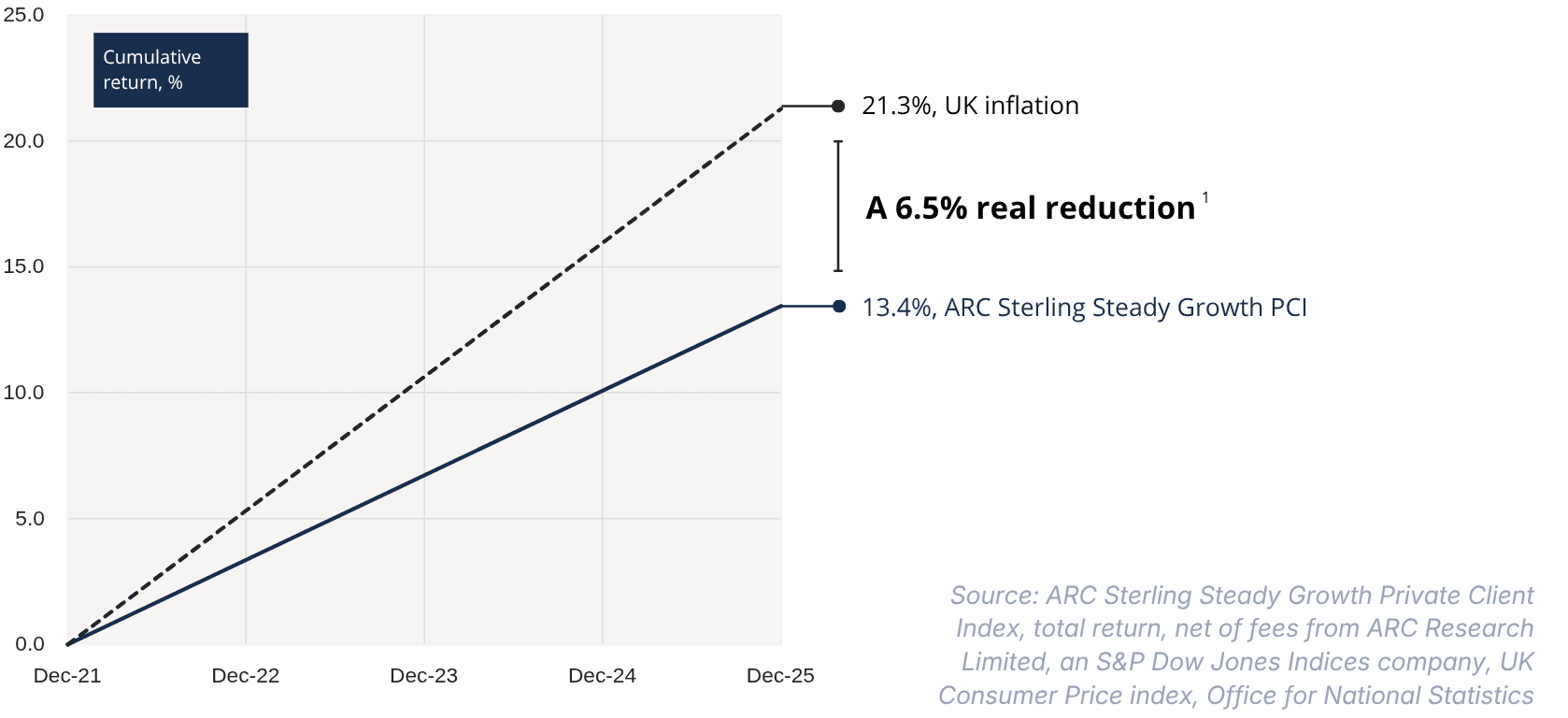

Since the beginning of the post-Covid-19 period however, returns of Sterling Steady Growth investors have lagged target returns of inflation plus 4%. Inflation during this period has been considerable and indeed on a real basis portfolio values have failed to keep pace. In real terms portfolio values are close to their all time highs but still 6.5% below their year end 2021 level and 7.9% below their August 2021 peak.

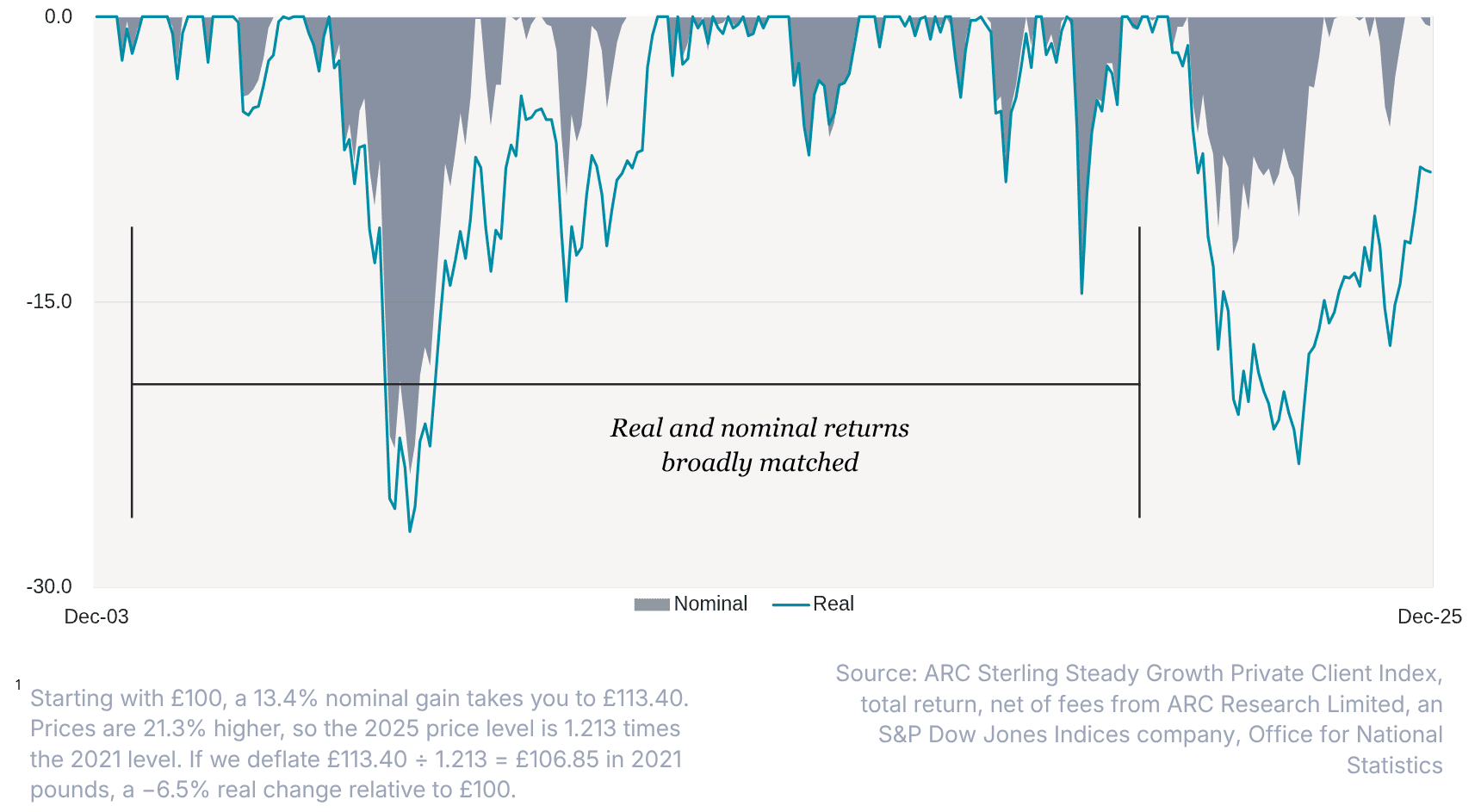

For decades investors have enjoyed low inflation and a focus on nominal returns has broadly matched the real experience. The drawdown chart below shows the mis-match between real and nominal returns and how significantly wealth has been impacted in the 2022 post-Covid-19 period.

2026: known unknowns

We can list many of the risks we see. Yet history suggests surprises bite harder. Our baseline is that client portfolios we oversee are built to weather shocks from many of the themes below.

The job is to keep resilience high and complacency low. While investors may wish for no surprises, being prepared for a few is wiser.

Elections

In the United States, all 435 House seats and 35 Senate seats are on the ballot on Tuesday 3 November 2026, alongside a large slate of gubernatorial and state races. With narrow margins, relatively small swings can change control, alter committee chairs and reset the policy agenda for 2027 to 2028.

Historically, the president’s party tends to lose House seats in midterms. That pattern is not a law of nature, but it is common and often priced into markets ahead of time. In practice, markets tend to fret before voting and find their footing after results reduce uncertainty, though macro conditions can dominate any electoral effect.

Jerome Powell’s four‑year term as the Fed chair ends in May 2026. The President will nominate the next chair and Senate confirmation will follow. Year end reporting suggested that a decision on the nominee was expected early in 2026, while Powell’s governor term runs to 2028, affecting the Board’s composition if he stays. Policy is made by committee, so the voting line‑up and incoming data will matter as much as the name on the chair. Investors want no surprises from the hand‑off. The committee vote and the data will be the real reveal.

Beyond the United States, there are more than 40 national‑level ballots scheduled around the world in 2026.

Brazil’s general election is on 4 October with a possible 25 October run‑off.

Hungary is expected to vote in April.

Colombia holds its presidential vote through May and June.

Taiwan

China continues to lay claim to Taiwan, stating that unification is unstoppable. The self‑governing island remains central to advanced chipmaking and therefore to AI, smartphones and data‑centre build‑outs. Most cutting edge capacity is still on the island, even as diversification progresses in the United States, Japan and Germany.

The People’s Liberation Army has run increasingly large military drills around Taiwan, including live‑fire exercises and blockade simulations.

The “silicon shield” idea persists for a reason, but it is not a guarantee. Investors should assume periodic tension, contingency planning and the possibility of short‑lived disruptions rather than bet on a single outcome. The knock‑on impact of any supply trouble on other industries would be substantial.

AI: enthusiasm, underweights and the bubble question

The top AI names drove index returns in 2025. Big Tech has signalled continued heavy capital expenditure for 2026, which can underpin orders yet raises the risk of over‑build if monetisation lags. Many active managers are underweight the AI complex after a period of underperformance against concentrated indices, which itself can fuel sharp catch‑up flows if earnings continue to surprise.

Earthquake risk and catastrophe bonds

Japan’s seismic advisory panel kept attention on the Nankai Trough by raising the 30 year probability for an magnitude 8–9 event to around 80% early in 2025, then later presenting a wider 60–90% range to reflect model uncertainty. In the San Francisco Bay Area, USGS continues to cite a 72% probability of a magnitude 6.7 plus event within 30 years. Those statistics are long known, yet they are a reminder that tail events cluster and model error is real.

Against that backdrop, catastrophe bonds have boomed. 2025 set issuance records and took outstanding notional above USD 60 billion. Spreads compressed through much of the year as capital chased yield and structures evolved. It looks attractive compared with recent experience. But quake peril remains a peak loss driver and Swiss Re’s sigma work underscores how quickly insured losses can run above trend in bad years. In plain English, cat bonds may carry more risk than backward‑looking data suggest when you are unlucky on timing.

Macro backdrop

The IMF’s October outlook has global growth easing to 3.1% in 2026, with inflation lower but not fully back to target in some economies.

The BIS highlights vulnerabilities in a world of higher real rates, heavy public debt and financial fragmentation. Those are the conditions in which known shocks sting and unknown shocks can amplify, another year when no surprises is a wish more than a forecast.

Closing thought

Markets will enter 2026 with headlines about indices at all‑time highs. In nominal terms that is true. Once adjusted for prices, the recovery proves illusory. The inflation pulse that followed the pandemic has eroded purchasing power to such an extent that portfolios remain about 7.9% below their August 2021 real peak. What looks like progress in pounds is, in practice, recovery only in name.

The year ahead still carries known unknowns. Elections can shift fiscal gears. The US Fed chair hand‑off will matter, though policy will remain anchored in the data. Taiwan’s role in semiconductors is unchanged and AI will keep testing underweights. Catastrophe risk still refuses to sit neatly inside models. Hope for no surprises remains evergreen; experience suggests it is unwise to count on.

Portfolios built for resilience rather than celebration of nominal milestones are better suited to this landscape. The task is to protect against the unexpected, stay liquid, stay diversified and rebuild real wealth with patience.

This article is provided for information purposes only and does not constitute investment advice or a personal recommendation. ARC accepts no liability for any action taken or not taken in reliance on this content. Click here for regulatory information, third-party data terms and full disclosures.